1. What is this post about?

A piece Quantpedia published in May 2026: “Dual Momentum Allocation Between Physical Gold and Bitcoin.”

The idea is simple. It’s a strategy that rotates weekly between Bitcoin (digital gold) and a gold ETF (GLD, the real thing), holding whichever one is doing better.

-

Check every Wednesday at the close

-

Hold the one with the higher trailing X-week return (relative momentum)

-

If that return is negative, sit in cash and hold neither (absolute momentum)

-

An additional “volatility cap” trims the position when Bitcoin gets too wild

The performance the paper claimed: the 8-week version returned 79.9% annualized; the volatility-capped version delivered 12% per year with a max drawdown of only -12% — supposedly far more stable than simply holding Bitcoin (46% return, -77% drawdown).

It looked interesting enough that I wired it into my own quant system and tested it for real.

2. Reproducing it: the numbers matched, but the paper had an error

I first ran it over the same window as the paper (2018–2026).

- The benchmarks lined up almost perfectly (gold ETF: 18.8% in the paper / 18.4% in mine)

- The base strategy matched too (paper 64.7% / mine 67.6%)

- But the “volatility-capped” version refused to line up. The paper showed 12% annualized with a -12% drawdown; I was getting 32% and -18%.

When I dug in, I realized the “20% volatility cap” the paper specifies couldn’t mathematically produce those numbers. The figures only reproduced exactly when I set the cap to about 8%. It looks like a calculation slip — most likely √252 used where √52 should have been, somewhere in the annualization. In other words, the paper’s “20% cap” was actually behaving like an 8% cap.

Lesson 1: Even a paper from a well-known site doesn’t deserve blind trust. Reproduce it yourself.

3. Tested properly, it lost to just buying gold

The paper’s real weakness was its validation methodology. It looked at the 2018–2026 window only and concluded “8 weeks is optimal” — but that’s almost certainly overfit to that one stretch.

So I pushed the data back to 2014 (11.6 years, three-plus crypto cycles) and split it properly.

- Tune the strategy parameters only on the earlier window

- Quarantine the recent window — which contains the 2022 crypto winter — purely for out-of-sample validation

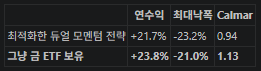

Results (2022–2026 validation window):

Even after optimization, the strategy lost on every single metric to mindlessly holding gold. The paper’s flashy results were an illusion that only held in one specific window.

(For the record, I also asked “would a shorter lookback do better?” — 3–4 weeks turned out to be slightly more robust than 8. The direction was right, but it still couldn’t beat just owning gold.)

4. Mixed with my own alpha, dynamic rotation added no value

Finally, I tried combining it with my own crypto alpha portfolio. Every possible mix of Bitcoin, gold, and my portfolio — sweeping across rebalance frequency and lookback length.

The verdict: rotating dynamically in and out of my portfolio added no value. A plain fixed 50:50 mix was better. Dual momentum’s whole point is “avoiding the bad asset” — but when one of your inputs is already a good strategy, there’s nothing to avoid, and committing 100% to a single asset just throws away the diversification.

5. The test that mattered most: what actually happened in the 2022 bear market

“When Bitcoin collapses, rotating into gold should cushion the fall, right?”

That’s the core hypothesis of this entire strategy. I checked it directly against the 2022 crypto winter (Bitcoin -77%).

The strategy didn’t survive the bear market. When Bitcoin collapsed, the strategy rotated into gold — but 2022 happened to be a rate-hiking cycle, and gold itself dropped -21%. When both assets fall, there’s nowhere left to rotate to. To its credit, the paper actually acknowledges this weakness in its own text.

Lesson 2: A “safe asset” isn’t always safe. Even gold wasn’t safe in 2022.

6. Wrapping up

The conclusions from all three layers of testing (reproduction → long-horizon, multi-window validation → combination with my own strategy) were consistent.

- The paper reproduces — but the paper has a calculation error.

- Tested honestly, it loses to just buying gold. The flashy returns were the illusion of overfitting one window.

- Mixed with my own alpha, the dynamic rotation didn’t help.

In the bear market, gold failed to defend. The very premise of the hypothesis came apart.

A fun idea, but not worth deploying.

Still, a meaningful exercise — another reminder that a “famous” strategy doesn’t earn your trust without verification.

댓글