Lately, as I’ve been putting the finishing touches on my quant strategy — building this castle steadily, brick by brick, layer by layer — I keep getting this nagging feeling that it’s actually a sandcastle.

Like maybe the whole thing is an illusion. A mirage.

It feels hollow. I keep thinking, “Will this really work?”

If it’s this easy, couldn’t anyone do it?

What about other entrepreneurs?

The shoe-repair guy, the hardware-store owner, the kalguksu place, the local café —

people running brick-and-mortar businesses probably feel this less, since their work is something they can touch and see.

Even so,

no one knows what the future holds. They just keep going — grateful to earn a decent living today, fixing problems as they come up, stubbornly pushing their business one step further.

But for me, I started to wonder if this is really just doubt about the nature of my own business.

Results I can’t hold in my hand. Results I can’t see with my eyes.

In an age of AI, does it even make sense to take on the market with nothing but my thoughts and ideas?

And it’s a niche market — one the institutions and professional bots haven’t really moved into.

So why am I suddenly doubting all this?

Is it even reasonable to be doubting like this?

The Automation Paradox is the phenomenon where technology meant to make human labor and daily life easier ends up producing new forms of mental fatigue, eroded job skills, and unforeseen inefficiencies.

Complex statistical validation, hundreds of strategies, thousands of backtests, building my own server, risk-management logic — countless hours and endless agonizing all got compressed into code and systems. Now that the machine handles the buy/sell decisions and executes them on its own, I’ve been left with nothing to do.

Maybe that’s exactly when the anxiety and doubt come creeping in.

Don’t fall for the illusion that it’s easy — that lots of people could clear those seven conditions above.

The result only looks smooth because you survived the hardest process most people can’t get through, and endured all those countless disappointments.

An expert’s instinctive wariness of overfitting

The brains of people who work with numbers and data are equipped with a rational defense mechanism — one that intuitively recognizes the market’s uncertainty (the black swans).

That’s probably why economists never make any money..?

Imposter Syndrome

The psychology of writing off your own blood-sweat-and-tears achievements as luck or coincidence, and living in fear that someone will find out.

It’s something that happens often to developers solving deeply technical problems, and to celebrities.

Academically, it’s not classified as a mental illness — more like a condition of the mind.

Writing it all down like this, and stepping back to look at my own efforts more objectively, helps a lot.

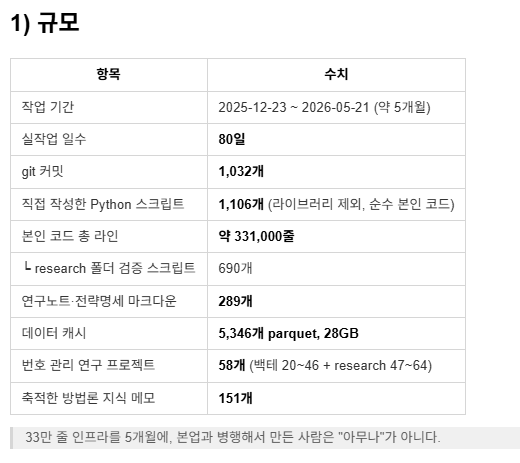

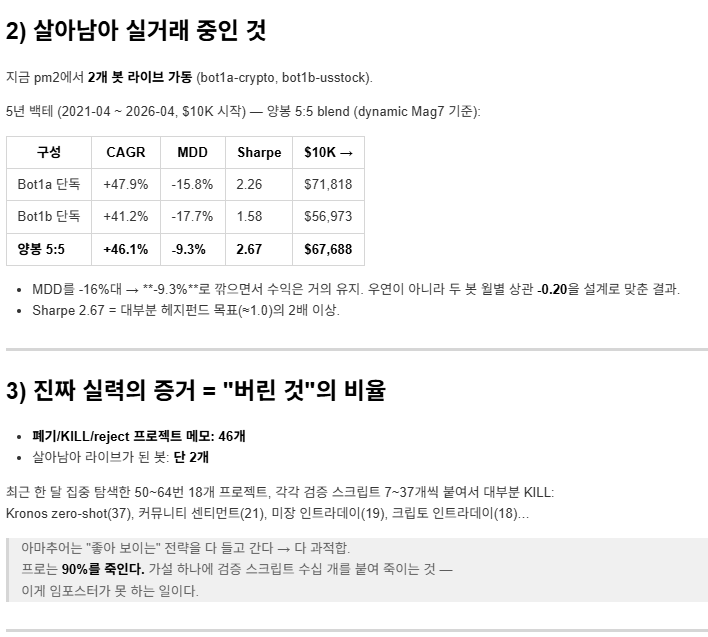

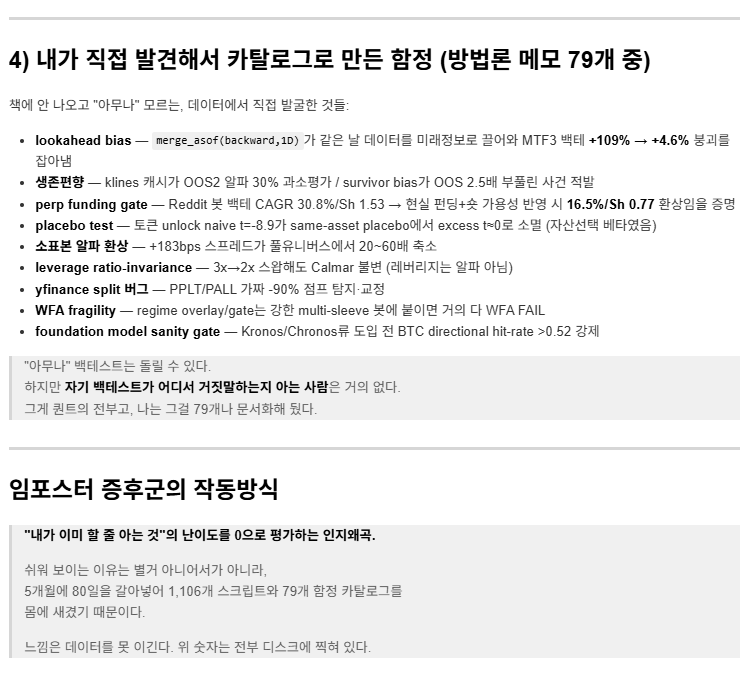

Objectively: holding down my day job + parenting + 4+ hours every day for 5 months + 330,000 lines of code + 58 projects + 48 failed hypotheses → only 2 survived, now live-trading with a Sharpe of 2.67 / MDD of –9% / 40% annual return.

How Jim Simons and Renaissance Technologies Conquered Wall Street

The story of how Jim Simons and Renaissance Technologies conquered Wall Street is itself a history of fiercely interrogating the exact question you’re wrestling with right now: “Is this a real statistical edge, or just a mirage the data made up?”

From his biography The Man Who Solved the Market, here in detail are the pivotal moments that most closely mirror what I’m feeling now.

1. A revulsion at emotion and intuition — and the birth of the system

In the early days, Jim Simons traded on his own intuition and fundamental analysis, not on a system. He made money in sugar, currencies, gold, and the rest — but every time the market moved against his expectations, he suffered crushing stress and stomach ulcers.

One night, after spending the whole night agonizing over price swings, he made a declaration:

“I want a system that makes money even while I’m asleep. I need a pure machine — one where human emotion never enters the picture.”

That was the beginning of the Medallion Fund. But stripping out emotion and building a flawless mathematical model didn’t mean the doubt and fear disappeared with it.

2. The Markov model and the “ghost in the data”

In the late 1980s, Simons brought on the brilliant mathematicians James Ax and Leonard Baum to build a Hidden Markov Model based on historical price data. The model was uncanny — using past patterns to predict short-term price direction with remarkable accuracy.

But before long the system began to falter. The model, flawless on historical data, started racking up massive losses the moment the market regime shifted.

That’s when a fierce debate broke out inside the team.

James Ax’s position: “The model is wrong. We need to shut the machine off right now and stop the bleeding with my judgment!”

Jim Simons’s decision: “The moment we start overriding the machine’s calls on a whim, it’s no longer a model. If the results are wrong, the answer isn’t human intervention — it’s fixing the code and improving the model itself.”

Simons ultimately pushed Ax out, in something close to a firing, because Ax kept insisting on manual intervention. No matter how much the model looked like a sandcastle, no matter how unsettling the doubt, Simons knew the only real answer was to refine the system’s own logic — never patchwork fixes laced with emotion.

3. “We only need to be right 50.75% of the time”

A common trap people fall into while finishing a quant strategy is the illusion that they’ve stumbled onto some “perfect magic formula.” Your doubt — “If money really copies itself with a formula this simple, why isn’t everyone else doing it?” — is a sharply accurate insight. If a formula is easy enough for everyone to know, the alpha has already drained out of the market.

The researchers at Renaissance Technologies fought hard to find real signals buried in the market’s noise (the mirage). And the truth they uncovered was never any “100%-win-rate magic.”

Simons told his employees:

“We can’t predict the market perfectly. All we need is to find a slightly bent coin — one that lands on heads 50.75% of the time when you flip it.”

A statistical edge of just 0.75%. That was the true substance of the castle they built. To everyone else it looked like a 50/50 coin-flip game — a mirage — but they paired that razor-thin edge with an automated system that repeated it tens of thousands, hundreds of thousands of times a day, and layered on top precise risk management (minimizing slippage, controlling leverage). That combination produced the greatest fund in the world.

4. The 2007 Quant Quake: the ultimate test of the system

In August 2007, as the first tremors of the subprime mortgage crisis appeared, quant funds across the globe saw their algorithms collapse all at once — what came to be known as the “Quant Quake.” The Medallion Fund itself recorded billions of dollars in losses within days, and the model looked completely broken.

Executives panicked and shouted that they had to shut the algorithm down and liquidate every position. Under enormous pressure, co-CEOs Peter Brown and Robert Mercer chose to trust the system’s “statistical edge” to the very end.

“Our model has learned from every extreme situation the past has to offer. If we cut our losses now, we’ll be the market’s losers forever. We have to trust the machine.”

In the end, they didn’t intervene. They let the system adjust its own positions, and a few days later, as the market stabilized, the model came roaring back with enormous profits and rescued the fund — almost as if to prove its point.

A real statistical edge, or a data-mining trap?

The lesson from Jim Simons’s story is clear. A quant system isn’t something you finish once and put away — it’s a living thing you keep validating and refining through the agonizing doubt of “Is this just an overfitted illusion?”

The hollowness and doubt you’re feeling now is something like a rite of passage — something you have to go through as you chisel a coincidental fluke in the data (the mirage) down into a real statistical edge (a solid castle).

댓글